-

![Profile picture of Editorals]()

Editorals wrote a new post

-

![Profile picture of Editorals]()

Editorals wrote a new post

“When you form a team, why do you try to form a team? Because teamwork builds trust and trust builds speed.” –Russel Honore

Ever since primary school all of us listen repeatedly about how important synergy in a

![Profile Photo]()

![Profile Photo]()

![Profile Photo]() liked this

liked this

-

![Profile picture of Editorals]()

Editorals wrote a new post

India faced an archaic type of government for a decade which systematically broke the backbone of Indians. Scams aggregating to millions of dollars left the state ex-chequer with a deep wound and undoubtedly pushed the development of our country several years or may be even decades back. Given the effect of time, inflation is bound to be factored in the price of every product and/or service. But a simple understanding of economics can make this thought clear in mind that if we did not have politicians and bureaucrats at different level of system, that amassed wealth at the speed a normal human breathes, India would not be facing such steep inflation figure, years of CAD, and weak consumer and business sentiments. 2G, Coal-Gate, CWG and many other scams which could have added funds to the nations account and eased the pressure of cross country payments as well as huge burden of domestic subsidy.

The UPA government subsidised rates on various utilities raising the debt burden of the country, which in actual terms is debt to every citizen to be repaid by additional direct and indirect taxes. The predecessors of Modi government had budgeted a whooping Rs.2.5 trillion (US$ 41 billion) on fuel, food and fertilizer subsidies for the fiscal April 2014 to March 2015. That’s almost 2.5% of GDP and 15% of total expenditure for the year. To put it in a nutshell, if a particular family gets all household utilities on leverage, the cycle has to stop somewhere. The suppliers will downgrade the credit rating of this particular borrower, the risk which India faced in late 2012 and early 2013 due to lack of reforms. One decade of chronic speed of development has made most of us so averse to taking leaps in taking the country forward. The country which jumped to a growth rate of 8.5% and a favourable CAD of 2.3% lost the focus when the power at the centre changed.

Domestic and foreign investors were averse to doing business in India as well as from entering Indian capital markets, due to lack of reforms which could come in near future. Amidst all these trivial issues, hopes started rising as Mr Narendra Modi was declared as the prime ministerial candidate. The news resulted in positive business sentiments not only in India but across the world and it started foreseeing reforms in India, and investment soared up immediately. Modi’s manifesto and speeches promised not only various upliftment policies of the poorer and weaker sections of the society but also focused on development in infrastructure and manufacturing sector. Although ,there is an empty chair of opposition and once in a while roaring Gandhi scion doesn’t seem to build strong counter arguments in parliament, NDA needs to work really hard to deliver what they promised.

Modi is less of a politician who will stick to the textbook shots and possesses thinking of more of a businessman who makes decisions and ensures execution of the same. BJP opposed FDI in multi retail which was proposed by the preceding ruling party but approved FDI in Defence and Railways. This is a classic example of a businessman who raises assets on leverage. Developmental and infrastructure projects will create job opportunities in domestic markets and increase the output of the country (Expected Unemployment for this year is 3.8% according to Global Employment Trends 2014). This will be done with foreign investment which will have systematic withdrawal plans. So when the investors pull out their money, we will be left out with infrastructure which will be of huge benefit to the people unlike FDI in multi retail which would drain the disposable income of Indians and take the invested amount as well as profits back home.

Indian markets are one of the favourite Asian markets which are in a bull period. Stock market reached record fresh highs on many occasions during pre and post-election result days. Almost 200 scripts were trading at 52 week highs on election results day i.e. 16th May 2014 on mere sentiments and speculation. Oil, Infra and banking sector stocks like Reliance industries, Adani Power, ONGC, Indian Oil Corporation, HDFC Bank, ICICI Bank were some of the heavy weights. PM’s “100 Days” agenda and independence day speech made the markets touch fresh lifetime highs on next trading day. Oil, auto and infrastructure sectors are the areas which will remain at higher levels due to policy reforms. 70% of the mid-cap and small-cap stocks which gave return as high as 75% to 200% between April to June period have fallen drastically and reached lower circuits in many day trades due to lower top and bottom line figures. Sales revenue of companies like NEPC India, Texmaco Rail, Quintegra Solutions, NIIT, etc were half in quarter ending June when compared to the same period a year ago. Traders had become active in fundamentally weak companies to take undue advantage of the positive sentiment all around Asia Pacific region.

Considering oil and fuel segment, petrol price reduced twice in a span of just 15days after a price cut in Mid-April 2014. Every US$ 1 decrease in crude oil price reduces around Rs.6000 Cr. Of India’s import bill. Crude oil was trading at US$ 112-113 on 10th July 2014, the day budget was announced which is US$ 10 higher from the current levels. International Crude oil prices of Indian basket went down to US$ 102.58 on 12th July 2014. If prices remain at US$ 103 levels, then it can reduce India’s oil import cost by Rs.60000 Cr. which is equivalent to budget of a bullet train. Oil Marketing Companies (OMCs) are now almost market driven company with book values of close to 3 compared to global players with book values of close to 5.5. Retail inflation was at two month high of 7.96% due to soaring vegetable and fruit prices factoring in weaker monsoon this year. This has eased with wholesale price index coming to a five month low at 5.19% and economists believe annual WPI will be around 5.10%.

While some stimulus needs to be to injected for economic growth to gain some momentum , economists don’t expect RBI to cut rates until 3rd quarter of next year as it has target of bringing down retail inflation down to 6% by start of 2016. So, RBI governor has to walk on a tight rope as he cannot reduce rates as core headline inflation figures are not getting any softer on the nation. Also any rate hike will dampen the growth prospect which seems to enter into a new dawn now after several months of negative and marginal growth numbers.Indian markets will be tested for its new resistance levels when the global interest rates rise and investments are pulled back. Also, the scenario worth waiting for is impact of PM Modi’s visit to USA in September and after talks between Indo-Pak foreign secretaries scheduled on August 25th have been called off. The most promising announcement seems to be of massive financial inclusion that the government is aiming for. It’s still a question whether dissolving Planning Commission and bringing in a new parallel structure will benefit the nation or otherwise. It’s only in hopes and in hindsight that people of India will know whether the new government, new PM and the market delivers and how.

About the Author:

Ronak Shah

He has completed PGDM (Financial Services) from K.J.Somaiya Institute of Management Studies & Research (2012-14) and is presently working as an Equity Research Analyst with Transparent Value.![]() Read More

Read MoreIndia faced an archaic type of government for a decade which systematically broke the backbone of Indians. Scams aggregating to millions of dollars left the state ex-chequer with a deep wound and undoubtedly pushed the development of our country...

![Profile Photo]()

![Profile Photo]()

![Profile Photo]() liked this

liked this

-

![Profile picture of Editorals]()

Editorals wrote a new post

![]() Read More

Read MoreWith the advent of technological innovation, life of mankind has changed significantly. Mobile phone is one such innovation that has brought all humans closer with their ability to talk, share and communicate. Now we have such a huge platform...

![Profile Photo]()

![Profile Photo]()

![Profile Photo]() liked this

liked this

-

![Profile picture of Editorals]()

Editorals wrote a new post

Xiaomi is the newest company to enter the highly competitive mobile device market in India. But does the staggering response on its Flipkart sale and a positive view by Indians indicate a conclusive future for![]() Read More

Read MoreXiaomi is the newest company to enter the highly competitive mobile device market in India. But does the staggering response on its Flipkart sale and a positive view by Indians indicate a conclusive future for the company in India?...

![Profile Photo]()

![Profile Photo]()

![Profile Photo]() liked this

liked this

-

![Profile picture of Editorals]()

Editorals wrote a new post

![]() Read More

Read MoreRwanda is a small, land-locked country located in east Africa. Bordered by Uganda, Tanzania, Burundi and the Democratic Republic of Congo, Rwanda has a population of over 12 million people. The major economic sectors are tourism, mining and agriculture....

![Profile Photo]()

![Profile Photo]()

![Profile Photo]() liked this

liked this

-

![Profile picture of Editorals]()

Editorals wrote a new post

Inflation has always been a worry and threat to every long-term investors. Any investment which is inflation-protected can protect investors from the loss of purchasing power that inflation can cause. In 1997, US first issued inflation-protected securities called Treasury Inflation-Protected Securities, or TIPS. TIPS are sometimes also known as Treasury Inflation-Indexed Securities. Credit risk and nominal interest risks are the two risks which have direct impact on investment decision of long-term investors for traditional fixed income securities. Investors can easily manage credit risk but nominal interest rate can’t be easily managed as it is difficult avoid the impact of inflation on securities. TIPS tries to overcome this by keeping pace with inflation as defined by consumer price index (CPI). TIPS are considered as extremely low-risk investments because they are backed by US government and their par value rises with inflation while their interest rate remains fixed.

TIPS can be purchased directly from government through Treasury Direct System (TDS). The minimum investment required is $100 with either 5-, 10- or 30-year maturities. Interest on TIPS are paid semi-annually. For example, let’s consider a $10,000-US TIPS was purchased with a 4% coupon. Also assume that inflation during the first year was 10%. So the face value of TIPS would adjust upward by 10%, to $11,000. As coupon payment (4%) is based on face value, so it is also adjusted and are paid $440 semi-annually. Hence both the bond’s face value and interest payments are protected against inflation. Thus TIPS protect investors from inflation but nominal bonds do not. But during deflation and negative inflation, nominal bonds are more attractive relative to TIPS because future interest payments become more valuable on a real basis. The trade-off between traditional and TIPS bonds is that latter offer much lower rates than traditional bonds. TIPS may have negative rates as investors may have to take a certain loss of purchasing power due to protection on inflation. Yields from conventional and TIPS bonds can be represented by following expressions:

TIPS Nominal Yield = Real yield + lagged actual inflation rate

Treasury Nominal Yield = Real yield + expected inflation rate + inflation risk premiumHow to purchase TIPS?

TIPS can be purchased in the same way as other fixed Income securities are purchased. TIPS can be purchased either directly as individual bonds through a broker / the US Treasury or owning the securities through mutual funds. Purchasing individual bonds are suitable for those investors who are seeking to match specific cash flow needs and purchasing bonds directly from Treasury is the best (cheapest) option for this. Buy and hold investors have advantage of purchasing TIPS directly as they can lock in a known real rate of return and a final maturity date. However, keeping TIPS directly creates problems for taxable investors as there are often mismatch between when adjustments to principal are taxed (current year) and when they are paid at maturity. Direct TIPS holders also face problems in reinvesting the semi-annual coupons in similar securities. Purchasing TIPS directly, however, allows investors to avoid the management fees associated with mutual funds.

Mutual fund can be the best option for the investors whose goal is to receive a fully diversified fixed-income portfolios of TIPS. Fixed income is important for investors of all sizes in the context of portfolio asset allocation. In the long run, fixed income securities have lower levels of return volatility but at the same time they also provide lower returns than equities. Investments in mutual fund provides investors to preserve the full purchasing power of assets involved in TIPS portfolios by automatic reinvestment of distributions. Investors of mutual fund of TIPS receive both the coupon and inflation adjustments in the same tax year. Thus, in order to maximize benefits from diversifications and to have proper exposure to assets, TIPS should be purchased through mutual funds. Purchasing TIPS through mutual funds for TIPS can add value over time by active management strategies.Who should invest in TIPS / Why TIPS

The benefits of investing in TIPS are:

1. Diversification Benefits:

TIPS play an important role in a diversified portfolio by providing a positive inflation –adjusted return for long-term investors. It’s a unique asset class that offers more opportunities to investors. For reducing the riskiness of the portfolio, TIPS play a major role. Although the fixed income securities provide lower returns than equities, but also provide much lower levels of return volatility and mostly helpful during the time of market stress when equities fall substantially.

Historically, TIPS have Low Correlation to Fixed Income and Equity Investments.

2. Low Risks

Conventional bonds are more risky than the TIPS. Thus, TIPS provide investors with a safer asset than has historically been available. As TIPS has only real interest rate risk, combining them with conventional bonds allows investors to disentangle inflation risk from real interest rate risk and thus to manage financial risk more efficiently.3. Lower Volatility Inflation Hedge

Among asset classes commonly used as inflation hedges, TIPS are the least volatile.Historically TIPS have Exhibited a Low Standard

Deviation of Returns

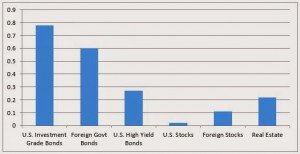

Asset Class

Annualized Return

Standard Deviation

Sharpe Ratio

TIPS

6.36%

6.20%

0.65%

U.S. Investment-Grade Bonds

5.21%

3.55%

0.82%

Foreign Govt. Bonds

4.77%

7.03%

0.35%

U.S. High-Yield Bonds

7.50%

9.84%

0.52%

U.S. Stocks

4.42%

15.51%

0.14%

Foreign Stocks

5.01%

17.65%

0.15%

Real Estate

10.71%

22.28%

0.37%

Commodities

6.18%

23.51%

0.16%

Factors affecting the demand of TIPS

Some of the factors that may affect demand for TIPS include:

▪ Inflation expectations

▪ Risk appetites

▪ Absolute real yield levels

▪ Flows into TIPS mutual funds

▪ Supply

▪ Expectation of strong CPI printsRates & Terms

TIPS are issued in terms of 5, 10, and 30 years. TIPS Inflation Index Ratios can be used to calculate the inflation adjustment to principal on previously issued TIPS. TIPS Inflation Index Ratio is defined as the ratio of the current CPI to the original CPI. TIPS can be held until maturity or sold before maturity.

TIPS Performance Factors

Return on TIPS is basically depends on two factors: real interest rate change and change in inflation.

Interplay of Interest Rates and Inflation

Changes in the interest rate impact the prices of the TIPS. But, unlike conventional bonds, TIPS prices are based on the real interest rates rather than the nominal interest rates and maturities tend to be longer. Inflation also impacts the performance. Positive inflation is good for TIPS and negative inflation is bad for TIPS. However, purchasers of TIPS in the secondary market or TIPS mutual funds must understand that the current market inflation expectation is already priced into the bond. Inflation ex-ante estimates must be less than the ex-post estimates to get benefited by the TIPS. Further, if inflationary pressures are causing rising rates, the picture becomes less clear.Unexpected Inflation

Real Interest Rates

Falling

Rising

High

Best

Uncertain

Low

Uncertain

Worst

Unexpected Nature of Inflation

Inflation is very difficult to predict. The predicted values are based on the historical data, which does not include the current economic scenario. Moreover, because of inflation, salaries and wages are raised which is taken as a positive factor, until the inflation eats the purchasing power. Because of this reason, it is better to include the securities protected against inflation to be included in the portfolio.Risks Associated with TIPS

Following are the risks associated with the TIPSType Of Risk

Explanation

Credit Risk

TIPS are issued by US government; therefore there is no credit risk.

Operational Risk

TIPS are not exposed to operational risk.

Market Risk

Not an issue for investors holding it until maturity. But, the moderate level of volatility has the potential to become an issue if the investor does not hold the bond till maturity.

Sovereign Risk

US government issued TIPS is having very low sovereign risk.

Liquidity Risk

TIPS are issued by US government; therefore there is no liquidity risk.

Interest rate Risk

Rare chance of deflation, or falling prices. This might occur during the depths of the financial crisis, when fears of a worldwide financial meltdown raised the possibility of deflation and led to a sharp decline in the prices.

Other Risk

CPI fails to track the actual inflation or the rising prices of products or services investor needs.

Impact of Taxes on TIPS

Income earned through investment is subject to taxes. Taxes do not differentiate between the real income and nominal income and re-exposed the indexed bonds to inflation risk. In the event of inflation and taxes it is possible that TIPS can have negative after-tax returns. All interest income and appreciation of the principal of an indexed bond are taxed as normal interest income, even though the appreciation of the principal only keeps the principal constant in terms of purchasing power. Even though the tax code brings inflation risk back to indexed bonds, the risk is small compared with nominal bonds. For every percentage point increase in inflation, the after-tax real yield on a nominal bond is reduced by a whole percentage point, while the after-tax real yield on an indexed bond is reduced only by the fraction of the marginal tax rate facing the investor of the bond.

Conclusion

Like conventional Treasury bonds, TIPS can decline in value over any short-term period. In other words, investors should not view a TIPS portfolio as a risk-free inflation hedge. To mitigate the impacts of unexpected and high inflation, investors should consider TIPS as a long term investment. In short term, both positive and negative real returns are possible. Given the current low-yield environment, the return outlook for TIPS is muted and likely to be more volatile than in the past. Nevertheless, the strategic case for bond diversification remains strong—including that for TIPS—given the uncertainty of the future inflation outlook. Clear understanding of the TIPS relation with inflation, interest rates and market expectations is important to make a well diversified portfolio. TIPS offer a lower volatility inflation hedging alternative. Many investors may find the features of TIPS mutual funds a more convenient way to invest in the asset class. The performance of TIPS during a rising rates period depends on the interplay of rising real interest rates, which negatively impact their prices, and unexpected inflation, which positively impacts their price. Bottom line, for long-term investors, including an allocation to TIPS is likely to improve diversification. As TIPS are one of the less volatile inflation hedges, they can be attractive to conservative investors.

About the Author:

Sumit Agarwal

He is presently pursuing his MBA from Indian Institute of Management, Ranchi with majors in finance and minors in Analytics, Operations and Marketing. Prior to this, he has worked in the steel industry for about 2 years.![]() Read More

Read MoreInflation has always been a worry and threat to every long-term investors. Any investment which is inflation-protected can protect investors from the loss of purchasing power that inflation can cause. In 1997, US first issued inflation-protected securities called Treasury...

![Profile Photo]()

![Profile Photo]()

![Profile Photo]() liked this

liked this

-

![Profile picture of Editorals]()

Editorals wrote a new post

![]() Read More

Read MoreComplexity has always pricked the brains of the best men throughout human history. Is there one unique way to define what complexity really means to organisms? In a utopian world, perhaps yes. It means different things to different areas...

![Profile Photo]()

![Profile Photo]()

![Profile Photo]() liked this

liked this

-

![Profile picture of Editorals]()

Editorals wrote a new post

![]() Read More

Read MoreTraditionally, Europe and America have enjoyed the continued dominance of Low Cost Carriers (LCC). Since 2003, a number of Low cost airlines have entered the Indian market. However, most of them are making losses largely due to high cost...

![Profile Photo]()

![Profile Photo]()

![Profile Photo]() liked this

liked this

-

![Profile picture of Editorals]()

Editorals wrote a new post

![]() Read More

Read MoreMe: What is the rate of the apple? Fruit Vendor: Rs.200/- per kg Me: But in the wholesale market, the rate of apples is Rs.120/- per kg Fruit Vendor: Sir, there in the wholesale market, you have to filter the good ones...

![Profile Photo]()

![Profile Photo]()

![Profile Photo]() liked this

2 Comments

liked this

2 Comments-

![Profile picture of Mohana Kodipaka]()

good article!! The fruit and vegetable vendors indeed apply several marketing principles which they have acquired through their years of experience in the market. 🙂

- Load More Posts

nice read