As of 30 March 2013, top 6 banks by market capitalization have been selected for the purpose of analytics in this report. All the data and statistics in the publication are primarily based on the annual reports and investor presentations retrieved from respective bank’ official websites. This report doesn’t endorse any bank or suggests investors to invest in particular bank.

Top six banks selected for analysis, as based on the market capitalization as of 30 March 2013, are: State HDFC Bank, State Bank of India, ICICI Bank, Axis Bank, Bank of Baroda and Punjab National Bank.

Performance at a glance:

Profitability

Banking Sector in India grew 15 percent in 2012-13 compared to 2011-12 as real GDP growth decelerated from 6.2 per cent to 5 per cent. Though overall banking industry managed to make a substantial profit this year, an interesting phenomenon was observed when the profit before tax of private and public sector banks were analysed individually. When top three private sector banks recorded increase of the order of 26.5 per cent in profit before tax, public sector banks, excluding SBI Bank who observed 7-8 per cent increase in their profit before tax, the other two public sector banks surprisingly recorded significant decrease in their profit before tax. This leads to net less than 1 per cent increase in profit before tax of public sector banks.

Another concern posing substantial threats to public sector banks in the coming financial year is the net interest margin. Net interest margin, the difference between interest earned on loans and that paid on deposits, is a key measure of a bank’s profitability. All PSU Bank under study witnessed substantial decrease in NIM as all their private sector counter parts were better off. The cost of deposits, though lower than what it was in April’12, has stayed in the higher slab as banks found it challenging to increase deposits, except in the last month of financial year.

In the economic slowdown scenario major hit was taken by public sector bank as they have lent largely to power, infrastructure and aviation sectors. This has also put an additional pressure on the asset quality of public sector banks whereas private sector banks managed to safeguard themselves against deteriorating asset quality, which is result of nonetheless the economic downturn.

Financial Performance

The banking sector performance is more closely linked to economy performance than any other sector in India. Indian economy witnessed downgrading from various significant rating agencies like S&P and also increasing Current Accounting Deficit. Private sector banks were better off than public sector bank also owing to the difficult business environment and decreasing credit growth. Moreover increasing stress on building internal credit appraisal mechanism from private sector banks have paid off and helped them to maintain their superior assets quality.

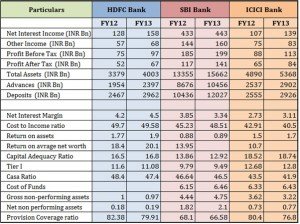

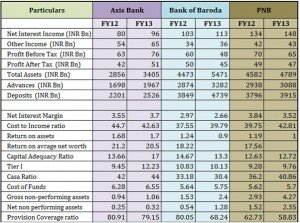

Net Interest Income

Net Interest Income, which is the difference between (a) interest payments the bank receives on loans outstanding and (b) interest payments the bank makes to customers on their deposits. Net interest income as a proportion of total income for the entire private as increased substantially i.e on average of 17-18 per cent whereas public sector banks could not register such similar trends. Such trends stem from the fact of incapability of having good assets. Moreover interest payments that banks make to customers have largely been on higher ide compared to y-o-y basis resulting in shrinking NII of PSBs.

Profit after tax (PAT)

Among all the banks under study, profit after tax also demarcated the PSBs and their private sector peers. When almost all private sector banks realised exorbitant profit after tax, PSBs, excluding SBI, witnessed substantial reduction in profit after tax. This trend is essentially prominent from the fact of higher provisions requirement dictated by Reserve Bank of India (RBI) compelling PSBs of India to bite the bullet and take up the challenge of competing with their private counter parts rather than boasting on large assets base.

Cost to income ratio (C-I ratio)

Cost to income ratio is a key financial measure, particularly important in valuing banks. It shows company’s cost in relation to its income. We derive at cost to income ratio by dividing (a) Operating Costs (such as administrative and fixed costs, such as salaries and property expenses, but not bad debts that have been written off) by (b) operating income. This ratio gives investors a clear view of how efficiently is the firm being run – the lower it is, the more profitable the bank will be. This indeed calls for an alarming stance on the part of PSBs whose C-I ratio has taken a major and crucial hit, especially when private sector banks exhibited decrease in C-I ratio. This could only be improved by PSBs by improving their operational efficiencies which would eventually result in reduction in their operational expenses. PSBs like PNB have marked a crucial escalation rate of the order of 5 per cent in salaries which will further damage their C-I ratio in the coming times. ICICI Bank outperformed all other banks by achieving reduction of the order of 5 per cent in C-I ratio.

Shareholders’ Returns

The past year was a challenging year for banking sector and stocks of Indian banks has muted performance owing to various macro-economic uncertainties, worsening asset quality, pressure on margins, aging workforce, and larger pension provisions, slowing down economy and tightening monetary policy.

The graph below shows the movements in the share prices of the banks under study during FY13.

As prominent from the graph, it can be clearly established that the trend of PSBs performing inferior compared to their private peers is also consistent with the shareholders’ return aspect. With the average growth of as high as 18 per cent in stock prices of Private sector banks, HDFC having recorded the highest growth of 21.5 per cent, the PSBs have actually witnessed the declining share prices resulting in the investment degradation and substantial shareholder’s losses. Excluding SBI, which has too observed a meagre growth of 2.5 per cent in stock price over the closer of previous financial year, Punjab National Bank and Bank of Baroda performance has only raised threatening concerns for investors and stakeholders which decline as huge as 12 per cent and 19 per cent respectively.

Dividends

Indian Banks have announced dividend along with their FY13 results varying in the range of 40 to 350 per cent. All six banks under study exhibit substantial dividend payout trend and increased amount over previous year, reflecting an increase of 11% to 22 per cent in total dividend payment in FY13. HDFC Bank declared a 30 per cent increase in the dividend of INR 5.5 per share against INR 4.3 per share in FY12. Highest dividend being paid by SBI of the order of Rs. 41.5 per share for FY13 as compared to Rs. 35 per share in FY12.

Financial Position

With the worsening economic outlook of Indian prime sectors and sinking macroeconomic factors, it becomes imperative for Indian banks to manage their assets portfolios cautiously and also allocate exorbitant amount as provisions for such weakening assets. Beyond this the regulatory requirements have emphasized on preserving capital requirements resulting in challenging operating environment for banks.

All banks under study displayed a one sided increasing trend in terms of total assets with highest increment realised on the balance sheet of SBI i.e more than 20%. It shows the various positive outcomes and moreover the inclination of banks to provide services to untapped market of India. The only point of concern during such figures is to develop an effective internal credit rating of assets before lending to them and falling prey to bad debts. Aggressive banking and business acquisition should not be realised at the cost of quality of assets.

Indian banks differentiate themselves in global front by maintaining diversified sources of liquidity to maintain flexibility in extending credit for diverse needs. Banks have options of getting deposits from either retail depositors or through corporate depositors for their incremental operations. Moreover banks may efficiently manage their liquidity by creating a strong asset liability management system (ALM) along with well-matched maturity patterns of assets and liabilities duration. Banks have found it difficult to maintain or increase their CASA deposits except Axis bank and PNB. It indicates a shift from CASA deposits to term deposits resulting in a decline in CASA ratio for all the rest of the banks, primarily driven by high interest rates offered by banks on term deposit than the corporate depositors. This will also enhance their cost of funds which is in line with the observation captured in number excerpts.

During FY13, both the Indian and global economies faced exorbitant challenges putting additional stress on asset quality eventually resulting in increase in GNPAs, net non performing assets and restructured assets. PSBs faced larger asset quality implications owing to the fact that they were the prime lenders to crucial and slowing sectors like power and agriculture which took substantial hit during the economic slowdown. On the contrary, relatively lower exposure towards these stressed sectors along with the adequate provisioning let to improvement in asset quality of private sector banks. All the PSBs under study registered phenomenal dip in quality assets and high increase in their GNPAs, as high as 50%. Private Banks on the contrary managed to keep their asset quality in check and could contain their GNPAs and rather improving on same in some cases. With the downgrading of Indian economy from various esteemed rating agencies and rupee depreciation, asset quality is only expected to assume trough over the canvass. Amid temporary improvement in GNPA, private banks couldn’t get away with the deteriorating NNPAs accumulating on their balance sheet. This factor exhibited completely uniform and worsening trend across all the banks under study.

RBI requires banks to maintain NPA coverage ratio of atleast 70.00 percent of GNPAs. However increasing NPAs have substantially brought down the NPA coverage ratios of banks to levels below 70.00 per cent.

With the Basel norms getting tighter, banks are now compelled to maintain healthy Capital adequacy which, for PSBs have been ensured largely by the capital infusion from the government side. Moreover Indian banks view to align themselves positively along with the Basel-III norms and guidelines by FY18.

All banks are compelled to maintain minimum 8.00 per cent Tier 1 capital adequacy. All the banks under study maintained the compelled norms when few of them also exhibit slight decline in the same. Axis Bank surprisingly stood different among the herd by showing substantial increase in their tier-I capital adequacy when banks like SBI and PNB actually faced slight decrease in their Tier-I ratio, though well above the compelling norms.

The future landscape

With the slowing down economy, Indian banks faces the following strengths and opportunities in the coming financial year which only time and macroeconomic factors would determine whether they could actually tap the opportunities or they simply fall prey to challenges and threats.

Downgrading of ratings on India to “BBB-“by S&P rating will affect the sentiments of investors and this in turn lead to stalemate in the economic activities and investments. Moreover weakening local currency, larger clearances issues, upcoming national elections and various policy and regulatory glitches would only keep foreign institutional investors and foreign direct investments at an arm’s length from our country which will eventually result in loss of business for banks.

Current account deficit has increased substantially which in turn would result in additional pressure on local currency aggravating situations for other macroeconomic factors which in turn would hit the economic and investment activities largely.

Other challenge which should be envisaged by private banks at this point of time should be the vision of our honourable finance minister, Mr. P Chidambaram, of creating a global sized bank as till date we do not have any Indian banks in top 30 and largest banks of the world.

Asset quality under deteriorating market conditions and investor’s sentiments would only be further damaged and banks would find it difficult to recover the amount lend out to various organizations and individuals.

Amid these challenges banks may also have various things to cheer up depending upon few initiatives. With the roll out of Aadhar Cards, Indian banks may act as an intermediary and may have benefit of having float over their operational aspect which would contribute to their bottom-line substantially.

Also introduction of goods and services tax would make bank better off with the larger float availability. With the implementation of Unique Identification Number, Indian Banks will play a pivotal role of intermediary and would have an access to larger float in exorbitant number of policy based execution.

New Banking licences, as offered by RBI, would only be seen as an opportunity for Indian Banks as the similar instances in the past have resulted in substantial balance sheet improvements of existing players whenever RBI floated and allotted new licences. Indian banking sector, like telecom sector, has witnessed positive impact of new players entering the market and hence this move would be appreciated and welcomed by Indian Banks.

With Quarter one results due soon, it will be interesting to see how are banks safeguarding themselves against deteriorating environment and at the same time trying to get hold of market share through their aggressive services and innovative products.