At a very conservative estimate, ATM transactions costs banks between Rs 5-10(this includes fixed costs like security/rent/infrastructure and variable cost of transaction processing/cash replenishment). But when the same customer directly swipes his debit card(on which many banks charge a nominal annual fee), the bank earns a commission of around 1%(the balance would go to the bank owning the Point of Sale device), without incurring significant costs. This in a nutshell, is the reason why banks are coming up with ‘free’ debit cards, ad & PR campaigns etc, all aimed at encouraging customers to swipe their debit cards. In a manner that would make any consultant proud, I could dig up the number of transactions/year, apply a random percentage of substitution and come up with a number that could make it to a glossy report or press release for a business magazine/newspaper.

But this presumes that debit cards will replace ATM transactions/cash withdrawals, and not cannibalize credit card transactions on which banks earn a slightly larger commission, and also interest for delayed payment. In fact, debit card replacing credit card transactions means that banks would lose the CASA(current accounts savings account) float, which is now around 2%-3%(i.e NIM). Therefore, I would expect banks to try mobile marketing/email to specifically target debit card promotions to those customers without credit cards of the same bank. Alternatively, the promotions could be for spends below certain amount so that it competes with ATM withdrawals, instead of cannibalizing the high ticket discretionary spends. But yes, if done right, these promotions could transfer consumer surplus to those banks strong in CASA/debit cards but not in credit cards. To avoid poor decision making like Bank of America’s effort in late 2011 to levy debit card fees(customers saw it as charging them for spending their own money)-a decision it eventually had to withdraw-banks should use behavioral finance and psychology considerations also.

Mobile banking on the other hand, is a different ball game. While the initial business models were focusing on the potential float income, the RBI put an end to that by mandating that the float balances would be held with a bank(not with the operator). However, the real goldmine is in the use of mobile banking to recharge prepaid accounts, rather than for mshopping. Presently, around 95% of Indian subscribers are prepaid(not sure about on value basis), and they recharge their accounts largely offline with banks paying the Point of Sale shopowners around 10% of the amount as commission. Given the small ticket size(say Rs 50-100), even those with access to net banking/credit card do not prefer to recharge it online unless given additional discounts, which telcos do not in fear of a backlash from their incubent POS distributors. But now, customers can put a one time deposit of Rs 1000-2000 from net banking/credit cards, and then use that amount for recharging their prepaid mobiles and for shopping. The telecom company heavily saves on prepaid mobile recharge, and also earns the commission(akin to debit card issuer bank) on that. And unlike debit cards, there is no fear of cannibalization also.

Both these things(debit cards and mbanking) have received heavy press coverage, but few articles I’ve seen have highlighted this point, or even the similarity between these prepaid business models, which survive on commissions rather than on float.

[The article has been written by Anandh Sundar Tripuri. He is an MBA from IIM Ahmedabad 2010-12 batch and a ranker in CA/CS/CWA exams. .]

You might like reading:

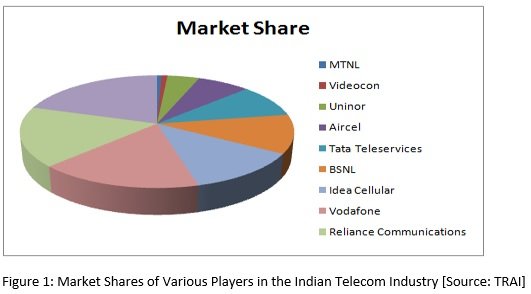

Analysis of the Indian Telecommunication Industry

The Indian telecommunication sector has emerged as a strong growth engine for the Indian economy in the last decade. Given the disruptive innovations and turmoil in this industry in the last decade, the typical Porter’s Five Forces cannot be used to analyze this industry. This article aims to study the industry using a modified Five Forces model, focusing on every […]

One Country… One Tax!

One Country… One Tax! There are three things that are difficult to understand in the entire universe. First two are Women, Duckworth louis’ system in Cricket and the third being GST. Before marriage, we give money to mother, father, brothers, sisters and friends. The condition will be different after marriage where we give our money only to our wife (GST). […]